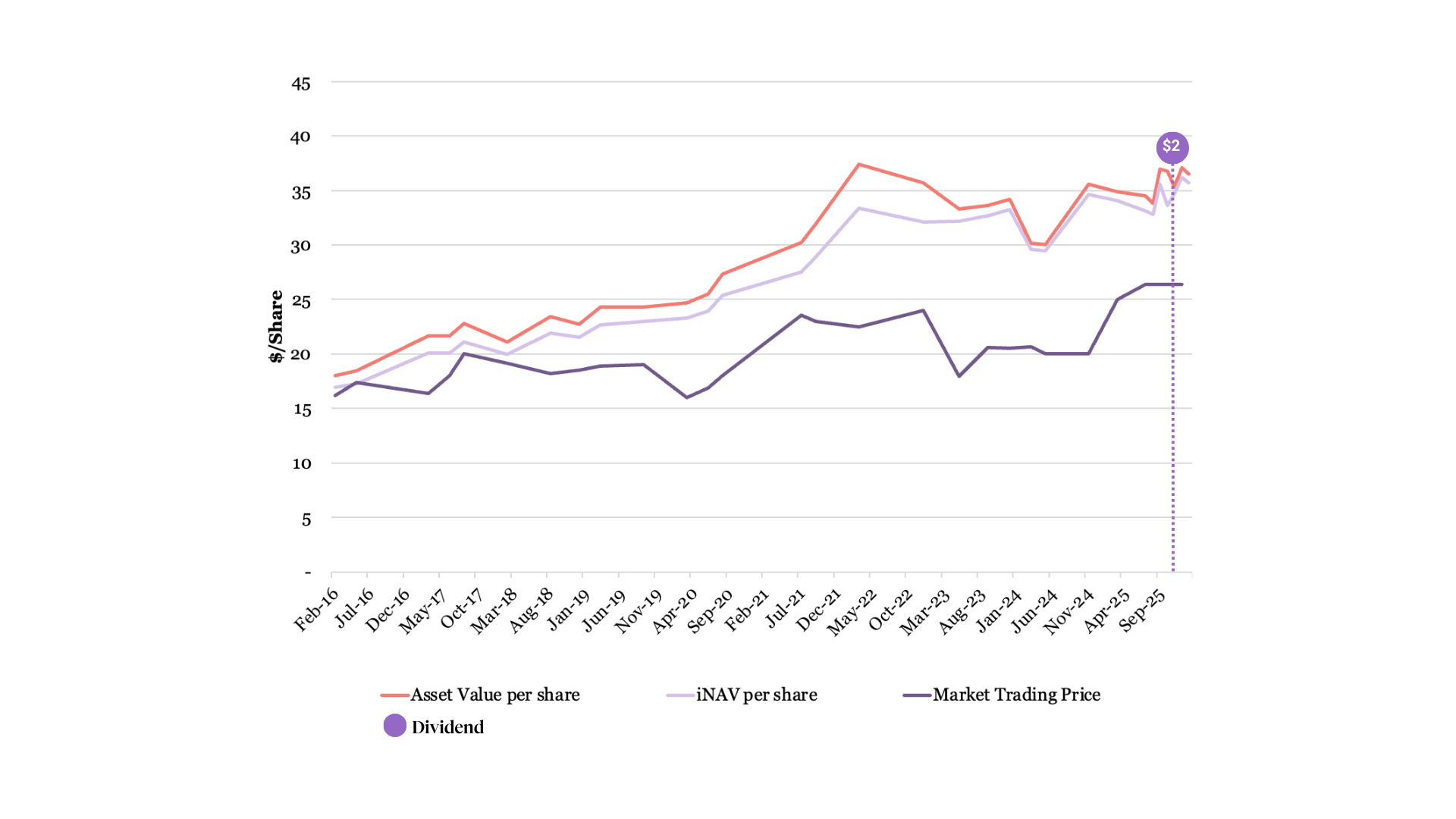

Your returns as a PFL shareholder are primarily determined by the price you pay when you buy shares and the price you receive when you sell them. In the meantime, the Investor Net Asset Value per share gives an indicative measure of the current value of your holding, reflecting the value of the portfolio minus any fees or adjustments.

*PFL’s policy is for the investment offer price to be within 5% of the Investor Net Asset Value per Share price.

* Noting that PFL’s share trading auctions may have limited liquidity and trade at discounts to the reported net asset value per share.

PFL’s evergreen structure is designed to deliver returns to investors via capital gains and for investors to realise their returns by selling their shares.

PFL is listed on Catalist Markets (a “recognised exchange” under New Zealand law) to enable shareholder liquidity and access. PFL currently offers 3-4 treasury stock-supported periodic share trading auctions on Catalist each year. Wholesale investors and existing shareholders can offer to buy or sell shares during these auctions. *

The fund has also been structured to keep open the possibility of a future NZX/ASX listing if the Board determines it in the best interest of shareholders. A listing is not assured.

* In the July 2025 trading window, roughly 1.2% of PFL shares traded on Catalist.

Existing shareholders and eligible/wholesale investors registered on Catalist can participate in periodic share trading auctions. If you are new to the platform, complete sign‑up and verification before the trading auction you wish to participate in begins.

One benefit of being an evergreen investment company is that PFL has a flexible toolkit for how and when to pass value on to shareholders.

Sometimes the value comes through share price / Investor Net Asset Value appreciation and liquidity events (you selling shares in share trading auctions), and sometimes through direct distributions, like dividends.

These choices are governed by PFL’s Capital Allocation Policy and are ultimately at the discretion of the Board. The Board’s decisions will factor in things like the fund’s cash needs for new investments, shareholders’ appetite for distributions, and fairness to all shareholders.

The Capital Allocation Policy determines how exit proceeds and portfolio‑company dividends are used: reinvested, distributed, or retained for reserves.

To improve the ability for shareholders to sell some of their shares during periodic trading windows, and to help align auction prices with PFL’s Investor Net Asset Value per share, the Board may authorise the fund to repurchase and hold up to 5% of shares on issue. Repurchased shares may be held as treasury stock under New Zealand’s Companies Act 1993, providing flexibility to reissue or cancel these shares later.

Any market support activity will be capped so that PFL does not hold any more than 5% of its shares at any one time, be subject to expenditure caps, executed under safe‑harbour practices, and reported transparently.